We are a blank check company incorporated as a Cayman Islands exempted company on January 19, 2021. We were formed for the purpose of effecting a merger, share exchange, asset acquisition, share purchase, reorganization or similar business combination with one or more businesses.

The Sponsor is Ross Holding Company LLC, a Cayman Islands limited liability company. The registration statement for the IPO was declared effective on March 11, 2021. On March 16, 2021, we consummated the IPO of 34,500,000 units, including 4,500,000 additional units to cover over-allotments, at $10.00 per unit, generating gross proceeds of $345.0 million, and incurring offering costs of approximately $19.9 million, of which approximately $12.1 million was for deferred underwriting commissions.

Simultaneously with the closing of the IPO, we consummated the private placement of 5,933,333 Private Placement Warrants at a price of $1.50 per warrant with the Sponsor, generating gross proceeds of $8.9 million.

Upon the closing of the IPO and the private placement, $345.0 million ($10.00 per unit) of the net proceeds of the IPO and certain of the proceeds of the private placement were placed in the trust account, located in the United States with Continental acting as trustee, and has been invested only in U.S. “government securities” within the meaning of Section 2(a)(16) of the Investment Company Act, having a maturity of 185 days or less or in money market funds meeting certain conditions under Rule 2a-7 promulgated under the Investment Company Act which invest only in direct U.S. government treasury obligations, as determined by us, until the earlier of: (i) the completion of a business combination and (ii) the distribution of the trust account as described below.

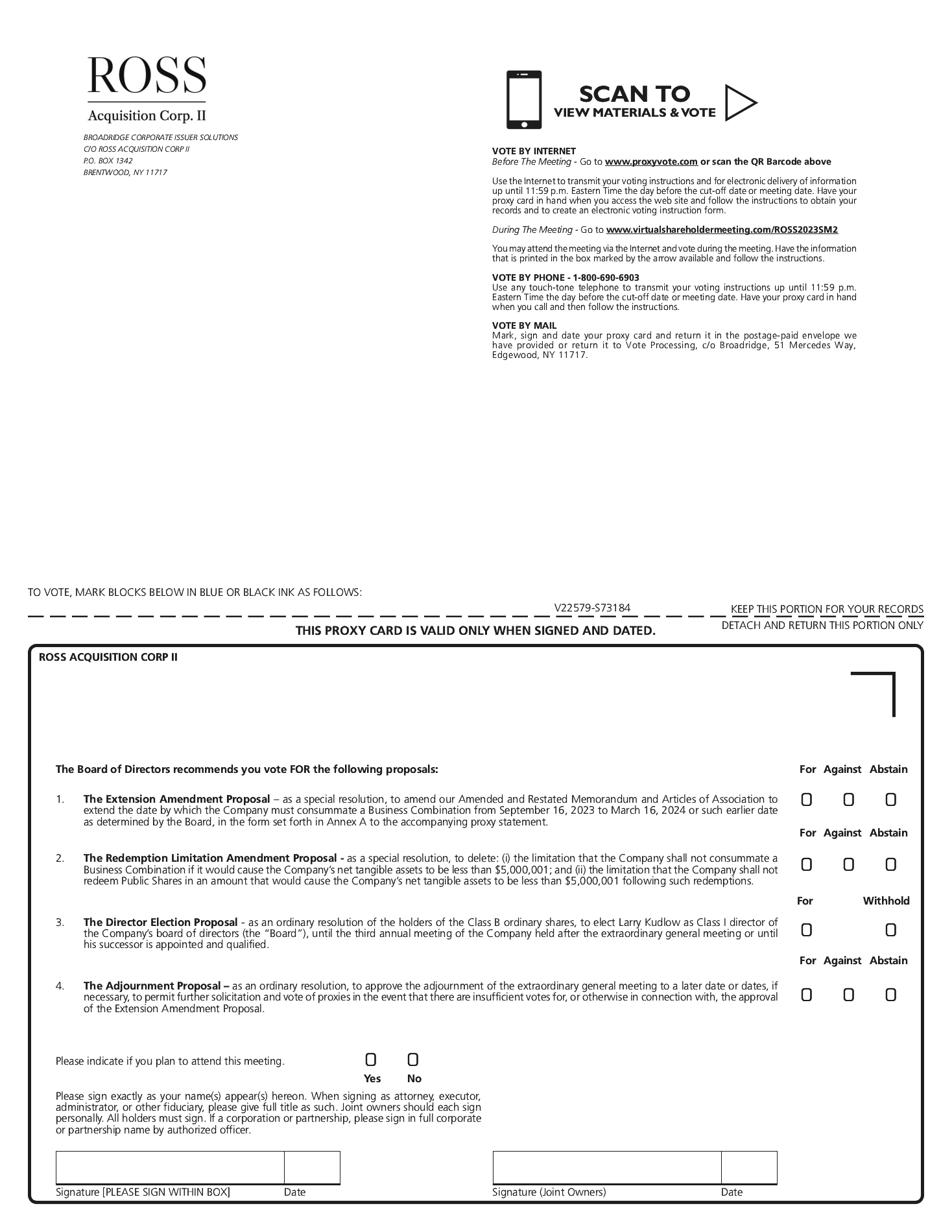

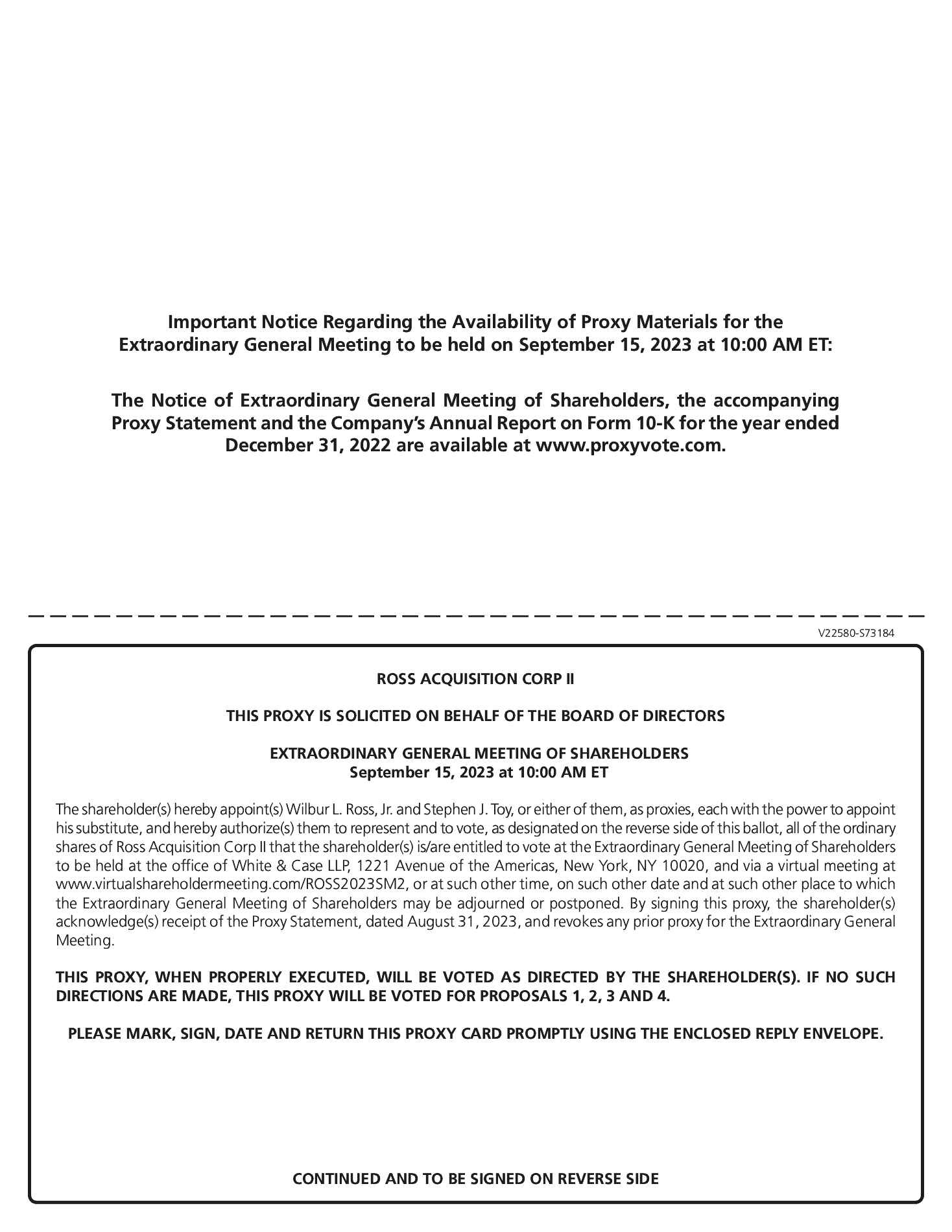

Like most blank check companies, our Articles provide for the return of the IPO proceeds held in the trust account to the holders of ordinary shares sold in the IPO if there is no qualifying Business Combination(s) consummated on or before a certain date. In our case such certain date was March 16, 2023, under our amended and restated articles of association dated March 16, 2021 (the “Prior Articles”), at the time of our IPO. On March 13, 2023, we held an extraordinary general meeting of shareholders (the “first extension meeting”), at which our shareholders voted and approved to amend our Prior Articles, which became our current Articles, to extend the date by which we must consummate a Business Combination from March 16, 2023 to September 16, 2023. In connection with the first extension meeting, a total of 28,119,098 Public Shares were presented for redemption for an aggregate redemption amount of approximately $287.7 million. As of the Record Date, the Company has approximately $68.6 million of cash remaining in the Trust Account.

If the Extension Amendment Proposal is not approved, or if the Extension Amendment Proposal is approved, but the Extension is not implemented, and we do not consummate a Business Combination by September 16, 2023 in accordance with our Articles, we will (i) cease all operations except for the purpose of winding up, (ii) as promptly as reasonably possible, but not more than ten business days thereafter redeem the Public Shares at a per-share price, payable in cash, equal to the aggregate amount then on deposit in the Trust Account, including interest earned on the funds held in the Trust Account and not previously released to the Company to pay its tax obligations, if any (less up to $100,000 of interest to pay dissolution expenses) divided by the number of the then-outstanding Public Shares, which redemption will completely extinguish Public Shareholders’ rights as shareholders (including the right to receive further liquidating distributions, if any), and (iii) as promptly as reasonably possible following such redemption, subject to the approval of our remaining shareholders and the Board, liquidate and dissolve, subject in the case of clauses (ii) and (iii), to our obligations under Cayman Islands law to provide for claims of creditors and other requirements of applicable law. There will be no redemption rights or liquidating distributions with respect to our warrants, which will expire worthless if we fail to complete a Business Combination by September 16, 2023, 30 months from the closing of the IPO. In the event of a liquidation, the Sponsor will not receive any monies held in the Trust Account as a result of their ownership of the Founder Shares or the Private Placement Warrants.

Our units, Class A ordinary shares and warrants are registered under the Exchange Act and we have reporting obligations, including the requirement that we file annual, quarterly and current reports with the SEC. The SEC’s internet site (http://www.sec.gov) contains such reports, proxy and information statements and other information regarding issuers that file electronically with the SEC. In accordance with the requirements of the Exchange Act, our annual reports contain financial statements audited and reported on by our independent registered public accounting firm.

Our executive offices are located at 1 Pelican Lane, Palm Beach, FL 33480 and our telephone number is (561) 655-2615. Our corporate website address is www.rossacquisition2.com. Our website and the information contained on, or that can be accessed through, the website is not deemed to be incorporated by reference in, and is not considered part of, this Proxy Statement.