of the Extension Amendment Proposal, the Board will retain the right to abandon and not implement the Extension Amendment at any time without any further action by our shareholders.

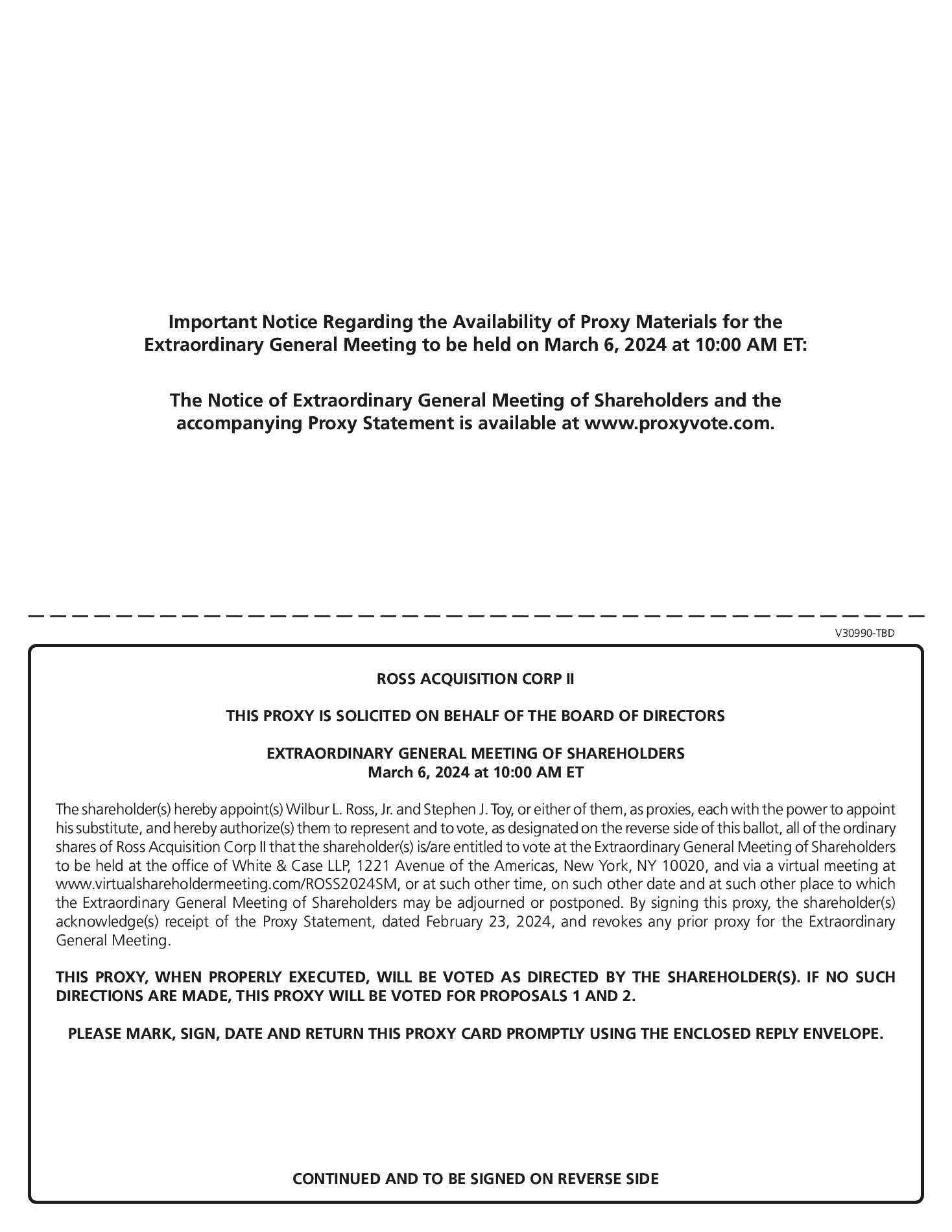

Shareholders who attend the extraordinary general meeting, either in person or by proxy (or, if a corporation or other non-natural person, by sending their duly authorized representative or proxy), will be counted (and the number of ordinary shares held by such shareholders will be counted) for the purposes of determining whether a quorum is present at the extraordinary general meeting. The presence, in person or by proxy or by duly authorized representative, at the extraordinary general meeting of the holders of a majority of all issued and outstanding ordinary shares entitled to vote at the extraordinary general meeting shall constitute a quorum for the extraordinary general meeting.

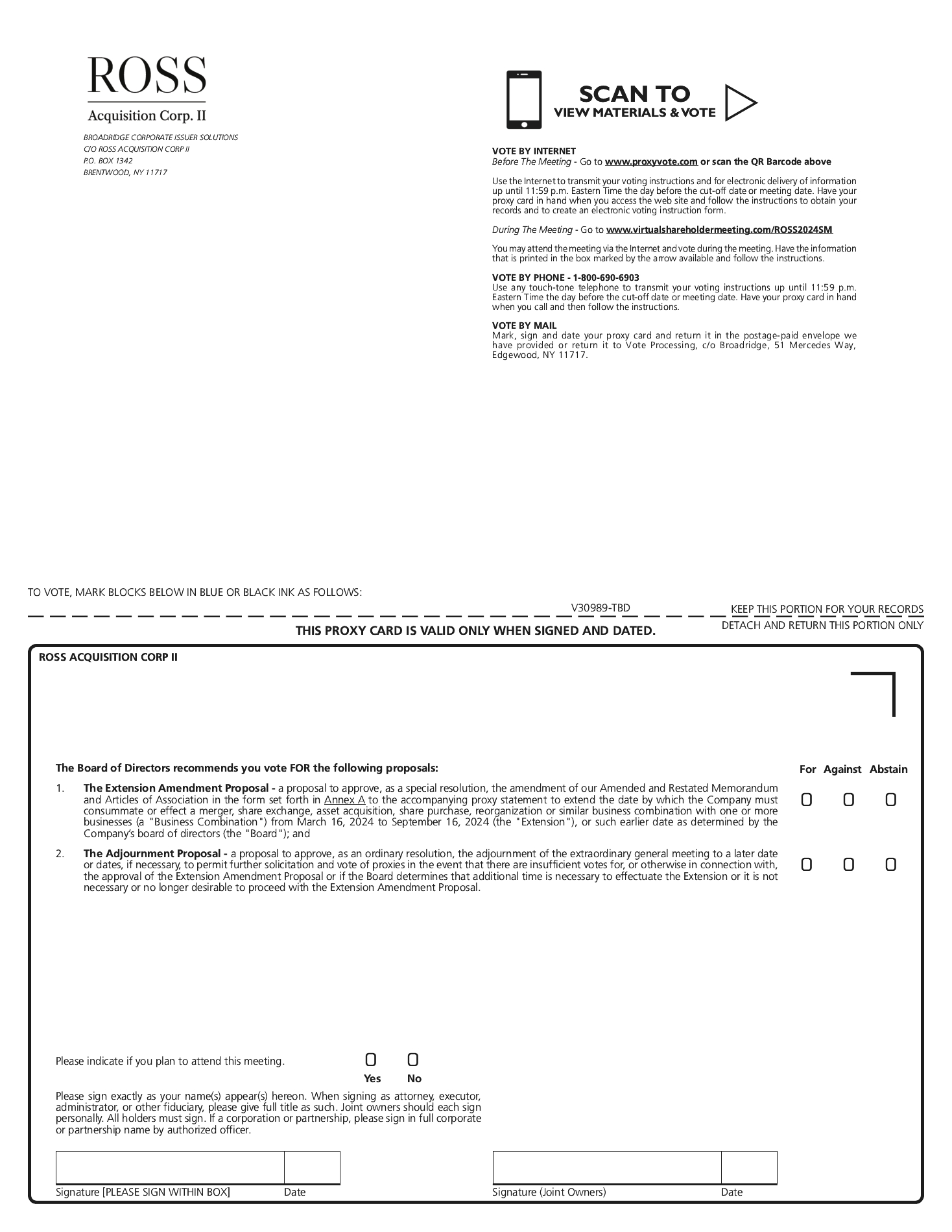

At the extraordinary general meeting, only those votes which are actually cast, either “FOR” or “AGAINST,” the Extension Amendment Proposal or the Adjournment Proposal, will be counted for the purposes of determining whether the Extension Amendment Proposal or the Adjournment Proposal (as the case may be) are approved, and any ordinary shares which are not voted at the extraordinary general meeting will have no effect on the outcome of such votes.

Abstentions and broker non-votes will be considered present for the purposes of establishing a quorum but, as a matter of Cayman Islands law, will not constitute votes cast at the extraordinary general meeting and therefore will have no effect on the approval of each of the Proposals as a matter of Cayman Islands law.

If my shares are held in “street name,” will my broker automatically vote them for me?

No. Under the rules of various national and regional securities exchanges, your broker, bank, or nominee cannot vote your shares with respect to non-discretionary matters unless you provide instructions on how to vote in accordance with the information and procedures provided to you by your broker, bank, or nominee.

We believe the Extension Amendment Proposal, and the Adjournment Proposal, if presented, will be considered non-discretionary, and therefore your broker, bank, or nominee cannot vote your shares without your instruction on these proposals. Consequently, your bank, broker, or other nominee can vote your shares for these proposals only if you provide instructions on how to vote. You should instruct your broker to vote your shares in accordance with directions you provide. If your shares are held in street name, you may need to obtain a proxy form from the institution that holds your shares and follow the instructions included on that form regarding how to instruct your broker to vote your shares.

How many votes must be present to hold the extraordinary general meeting?

A quorum of our shareholders is necessary to hold a valid meeting. The presence (which would include presence at the virtual extraordinary general meeting), in person or by proxy, of shareholders holding a majority of the ordinary shares entitled to vote at the extraordinary general meeting constitutes a “quorum.”

Your shares will be counted towards the quorum only if you submit a valid proxy (or one is submitted on your behalf by your broker, bank or other nominee), attend in person or if you vote online at the extraordinary general meeting. Abstentions will be counted towards the quorum requirement. In the absence of a quorum, the chairman of the extraordinary general meeting has the power to adjourn the extraordinary general meeting. As of the Record Date for the extraordinary general meeting, 6,833,050 ordinary shares would be required to achieve a quorum.

All of our directors, executive officers and their respective affiliates are expected to vote any ordinary shares over which they have voting control (including any Public Shares owned by them) in favor of the Extension Amendment Proposal, and, if presented, the Adjournment Proposal. Currently, the Sponsor owns approximately 63.1% of our issued and outstanding ordinary shares, including 8,625,000 Founder Shares. Accordingly, no additional Public Shares will need to be present for a quorum.

Who can vote at the extraordinary general meeting?

Only holders of record of our ordinary shares at the close of business on the Record Date, February 21, 2024, are entitled to have their vote counted at the extraordinary general meeting and any adjournments or postponements thereof. On this Record Date, 5,041,098 Class A ordinary shares and 8,625,000 Class B ordinary shares were outstanding and entitled to vote.